From Oct. 15 to Dec. 7, 2022, qualified participants can sign up to take part in the federal government’s insurance plan. If you are overwhelmed by the process, definitions and complexities of Medicare, you are not alone. According to the Centers for Medicare & Medicaid Services (CMS), almost 64 million Americans were fully enrolled in the Medicare program in October 2021. That’s a lot of medication and doctor visits. For those navigating enrollment this year, these are the key questions clients often ask.

When should I enroll in Medicare?

Most Americans enroll in Medicare when they turn 65. The Initial Enrollment Period (IEP) runs for seven months total – three months prior to your birth month, your birth month and three months after your birth month. For instance, if you were born in April, you are eligible to enroll January through July of the year you turn 65. During this time, you will have guaranteed acceptance for all Medicare plans, meaning you cannot be denied coverage for any reason for any part of Medicare. Once you sign up, your Medicare coverage will begin either on the first day of your birth month or the first of the month after you enroll after your 65th birthday.

Do I have to enroll in Medicare?

If you are still employed or receive health insurance through your employer’s plan, a spouse’s plan or a union group health plan and your employer has 20 or more employees, then you do not need to enroll in Medicare when you turn 65. You can wait until you officially terminate from your group health plan, either through retirement or loss of employment.

Medicare regulations require that anyone covered by a small employer plan with less than 20 employees must enroll in Medicare at age 65 instead of the group plan.

Which elements of Medicare do I need to sign up for?

There are essentially five main components of Medicare, and each serves a specific purpose. Here is a brief explanation of each component and some of the benefits they provide:

Medicare Part A – Hospital Insurance

- Coverage for inpatient hospital care, hospice care, inpatient skilled nursing facility and limited home health care

Medicare Part B – Physicians and Medical Tests

- Coverage for physician services, outpatient care, home health and medical services

- Provides coverage for some preventive health services

Medicare Part C – Medicare Advantage

- Coverage through a private insurer approved by Medicare

- Coverage provided through an HMO network

- Enrollment requires Part A and Part B enrollment

Medicare Part D – Prescription Drug Coverage

- Prescription drug coverage through a private insurer approved by Medicare

- Enrollment in Part D requires you to already be enrolled in Part A and Part B

Medicare Supplement/Medigap Plan

- Coverage through a private insurer approved by Medicare

- Plan covers the 20% coinsurance “gap” from Part B

- Eight standardized plan choices regulated by Medicare

- Enrollment requires Part A and Part B enrollment

While everyone who enrolls in Medicare will sign up for Parts A and B, you will need to make a choice on what other plans you will choose. For full enrollment of Medicare, you will choose one of two paths:

- Traditional Medicare – Parts A & B, a Part D plan and a Medicare Supplement plan

- Medicare Advantage – Parts A & B and Medicare Advantage (Part C) plan

How much does Medicare cost?

Your monthly cost for Medicare will vary depending on the type of Medicare coverage you choose, the specific plans you enroll in and your annual income.

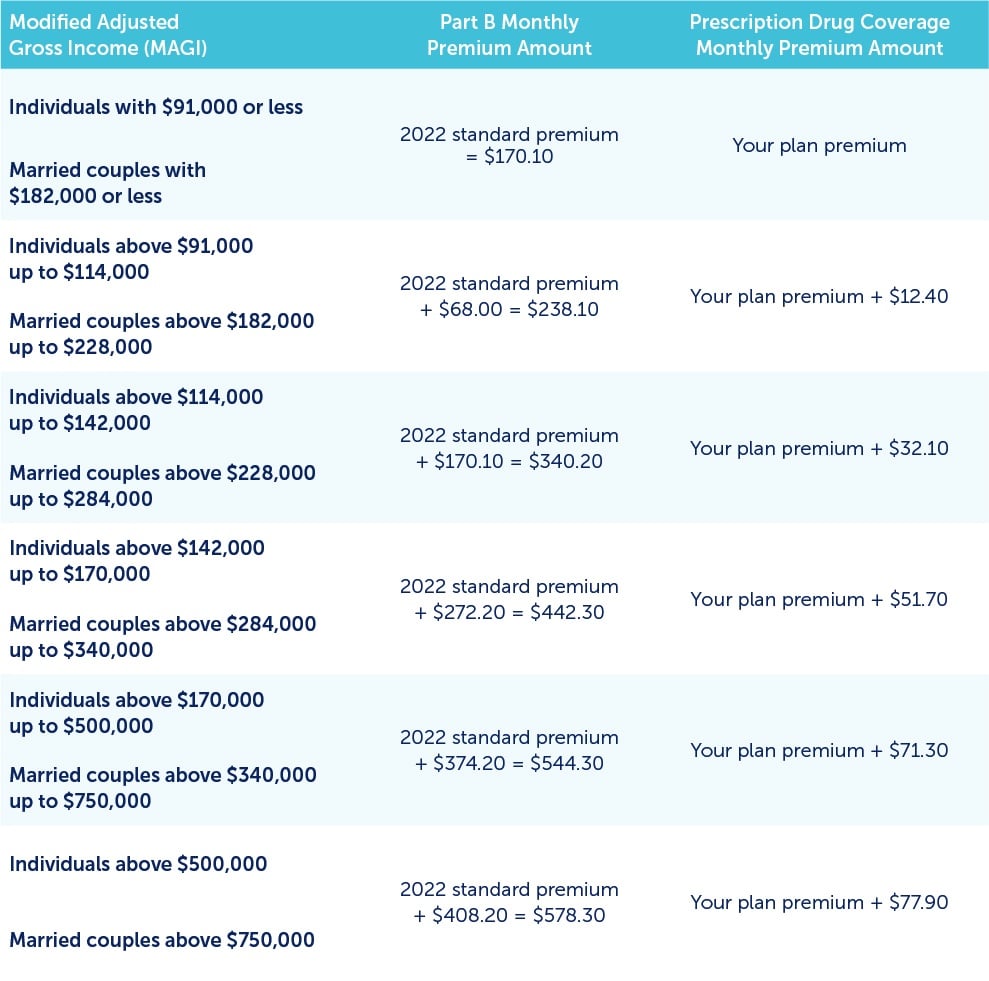

The good news is that for most people, Part A costs you nothing. These premiums are covered by the federal payroll taxes we pay. For Part B, the base monthly premium is $170.10 for 2022, and this applies to everyone on Medicare. Around November, new premium amounts will be announced by Social Security.

However, depending on your income, your Part B premium may be higher due to an Income Related Monthly Adjustment Amount (IRMAA). This is determined based on your income reported in your tax returns for the two prior years. If you earned over $91,000 those years and are enrolled in Medicare Part B and/or Part D, there will be a surcharge added to these elements. Social Security reviews your Modified Adjusted Gross Income (MAGI) each year, which is based on your income from the prior year, and reassess how much your Part B premiums will be for the upcoming year.

For couples who are married and file separately, the 2021 income tiers and adjustments are:

Once you have met the qualifications to enroll in Medicare, how do you sign up? The quickest and easiest way is online with the Social Security Administration at www.ssa.gov. You’ll need to create a “my Social Security” account prior to enrollment. You can also enroll by calling Social Security at 800-772-1213 or visiting your local Social Security office.

Your retirement shouldn’t be spent sifting through hours of red tape to receive the medical care you need and deserve. If you have questions about the facets of Medicare, please reach out to your advisor. Cheers to a healthy year!

About the author:

As an Onboarding & Integration Advisor, Scot Colgrove, CFP® enjoys breaking down complex issues to simpler, more easily understood concepts. He and his team lead training on the latest systems, processes and the firm to help new teams acclimate to Buckingham. He serves as an advocate for the joining firms whenever needed. His goal is to make the transition as anxiety free as he can for them.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party information and is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated other otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this information. 22-4422

The post The A, B, Cs of Medicare appeared first on Buckingham Strategic Partners.